Reverse Mortgage Requirements in California

Eligibility basics, financial assessment, property responsibilities, and counseling expectations.

Short answer

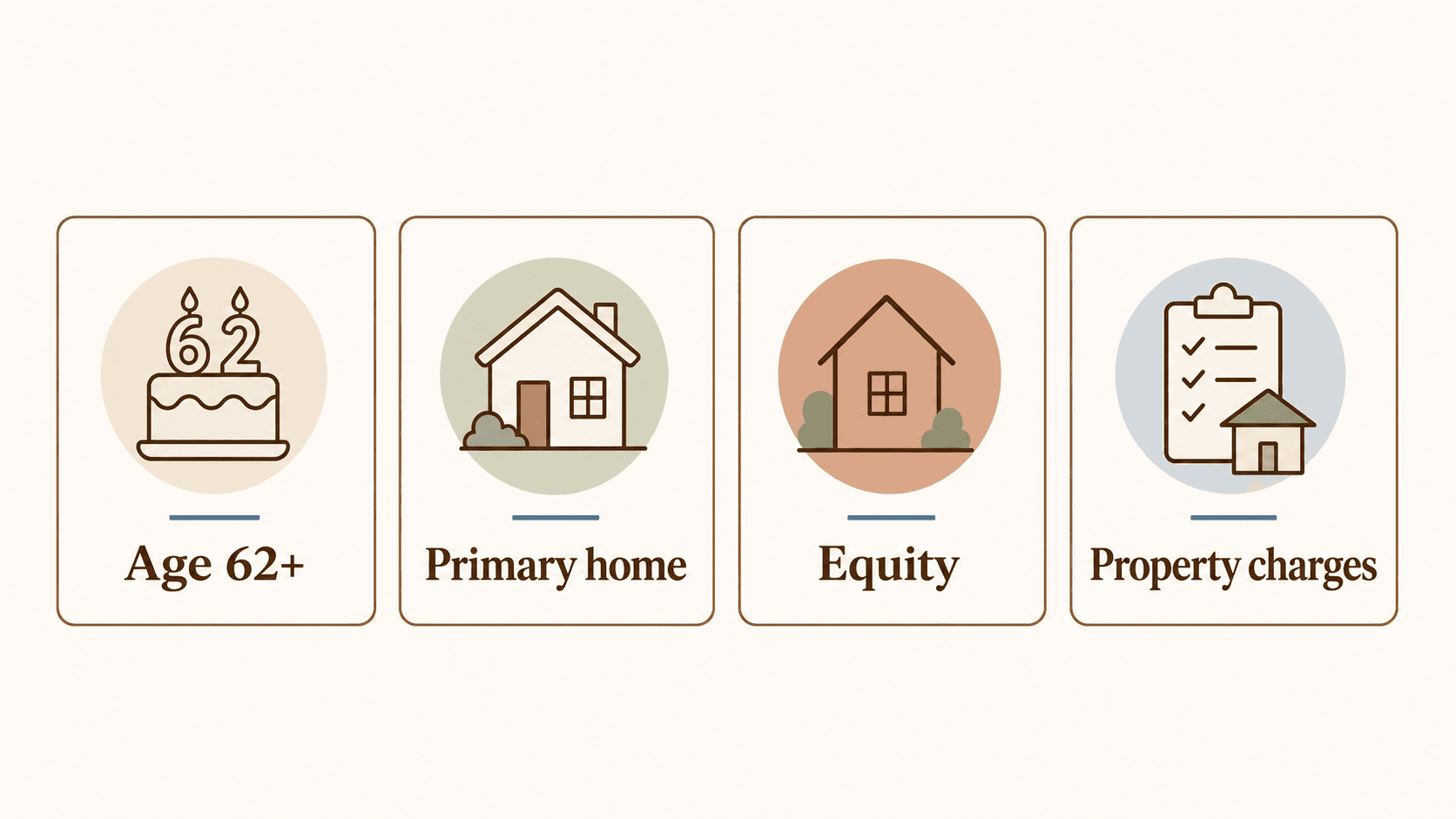

Core HECM requirements include age, principal residence, sufficient equity, financial assessment, property eligibility, and HUD-approved counseling.

What matters most in California

At least one borrower generally must be age 62 or older for a HECM.

The home must be the principal residence.

The borrower must complete required HECM counseling.

Financial assessment reviews whether the homeowner can meet ongoing property obligations.

Common misunderstandings

Age and equity alone do not guarantee approval.

Required property charges continue after closing.

Counseling is not the same as loan approval.

State context matters, but the core HECM eligibility framework is federal.

Questions to ask before applying

Is the home the borrower's primary residence?

Is there enough equity after current liens are considered?

Can taxes, insurance, HOA dues, and maintenance remain current?

Are there property or title issues that need review?

What requirements mean for California homeowners

California reverse mortgage requirements are mostly the federal HECM requirements: age, principal residence, equity, property eligibility, counseling, and financial assessment. The California conversation usually becomes local when the home value, family timing, property charges, and long-term housing plan need to be reviewed together.

Age and occupancy

At least one borrower generally must meet the HECM age requirement, and the home must be the borrower's principal residence.

Equity and existing liens

A high-value California home may have meaningful equity, but current mortgage balances, liens, and program limits still shape what is possible.

Counseling and financial assessment

HUD-approved counseling is required for HECM loans, and financial assessment reviews whether the homeowner can keep property charges current.

Issues that can slow down a reverse mortgage application

These are not automatic disqualifiers in every case, but they are the kinds of questions Ventana should surface early so a homeowner is not surprised later.

Property charges

Taxes, homeowners insurance, HOA dues when applicable, and maintenance remain the homeowner's responsibility after closing.

Family and title questions

California families often need to clarify ownership, heirs, trusts, adult children's concerns, and future sale timing before moving forward.

Timing

If a sale, move, care transition, or family decision is likely soon, the requirements conversation should include whether applying now makes practical sense.

Terms homeowners often ask about

Ask a question about reverse mortgage requirements in California

Share the situation you are trying to solve. Ventana can help you understand whether the next step is a calculator estimate, a family conversation, counseling, or a deeper review.

Lori will review your note and follow up with a practical next step.

Reverse Mortgage Requirements questions in California

What is financial assessment?+

Financial assessment is a lender review of income, credit history, property charges, and other factors related to the borrower's ability to meet ongoing obligations.

What is LESA?+

A Life Expectancy Set-Aside may be required in some cases to help pay future taxes and insurance when financial assessment shows additional support is needed.

Do property taxes still have to be paid?+

Yes. Property taxes, homeowners insurance, HOA dues when applicable, maintenance, and occupancy requirements remain the homeowner's responsibility.

Official reverse mortgage references

Ventana explains reverse mortgage options in plain language. Program details should be confirmed against current HUD, FHA, CFPB, lender, and counseling guidance before a homeowner makes a decision.

Have questions about a reverse mortgage?

Talk with Ventana before you make a decision. The first conversation is about clarity, not pressure.