HECM Loans in California

A practical explanation of the FHA-insured Home Equity Conversion Mortgage program.

Short answer

HECM stands for Home Equity Conversion Mortgage, the FHA-insured reverse mortgage program used by many eligible homeowners age 62 and older.

What matters most in California

HECM loans are insured by the Federal Housing Administration.

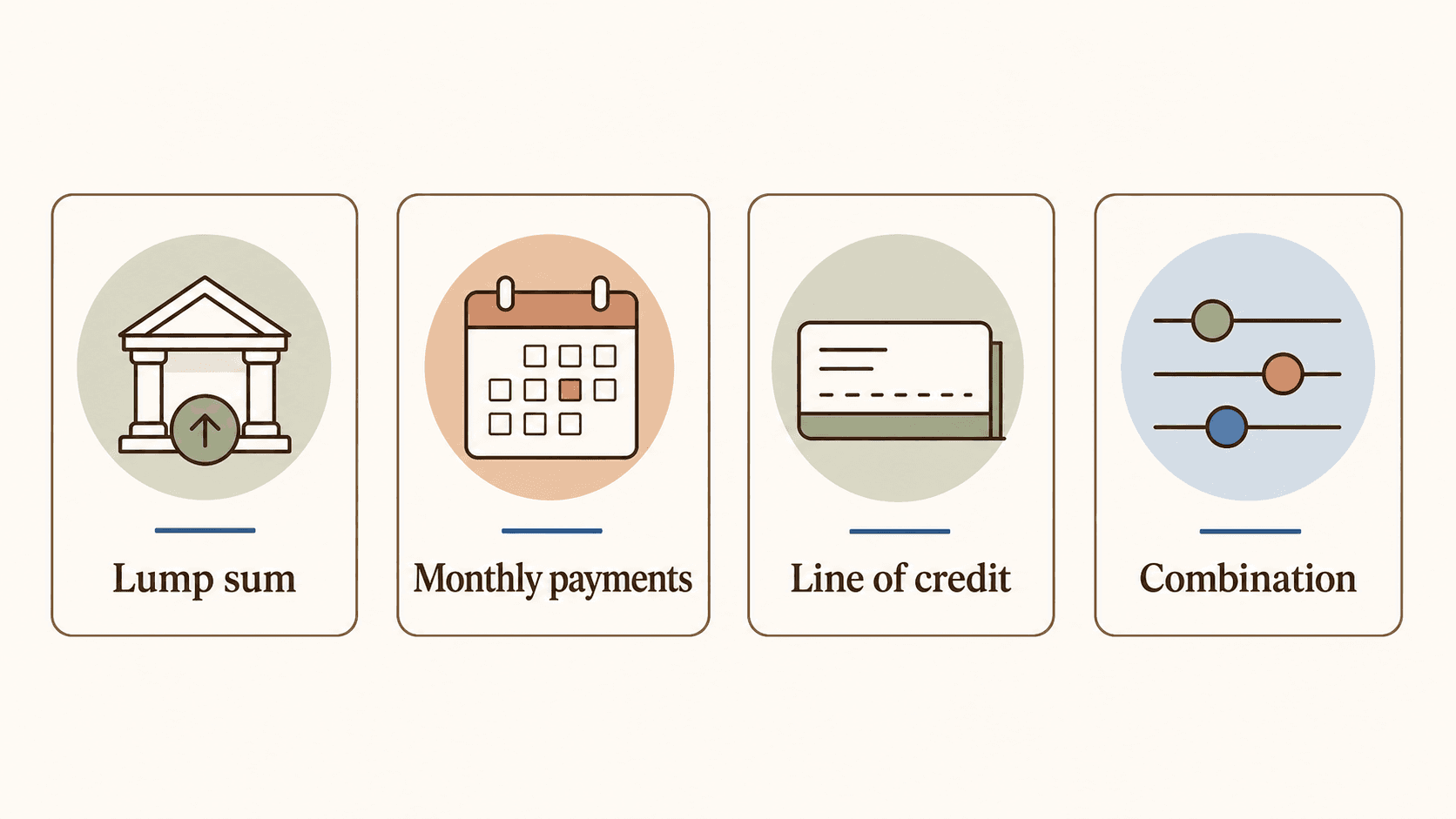

Borrowers can receive proceeds through options such as a line of credit, monthly advances, lump sum, or a combination, subject to program rules.

HECM loans are non-recourse, which generally limits repayment to the value of the home when the loan becomes due.

The homeowner must continue meeting occupancy and property-charge responsibilities.

Common misunderstandings

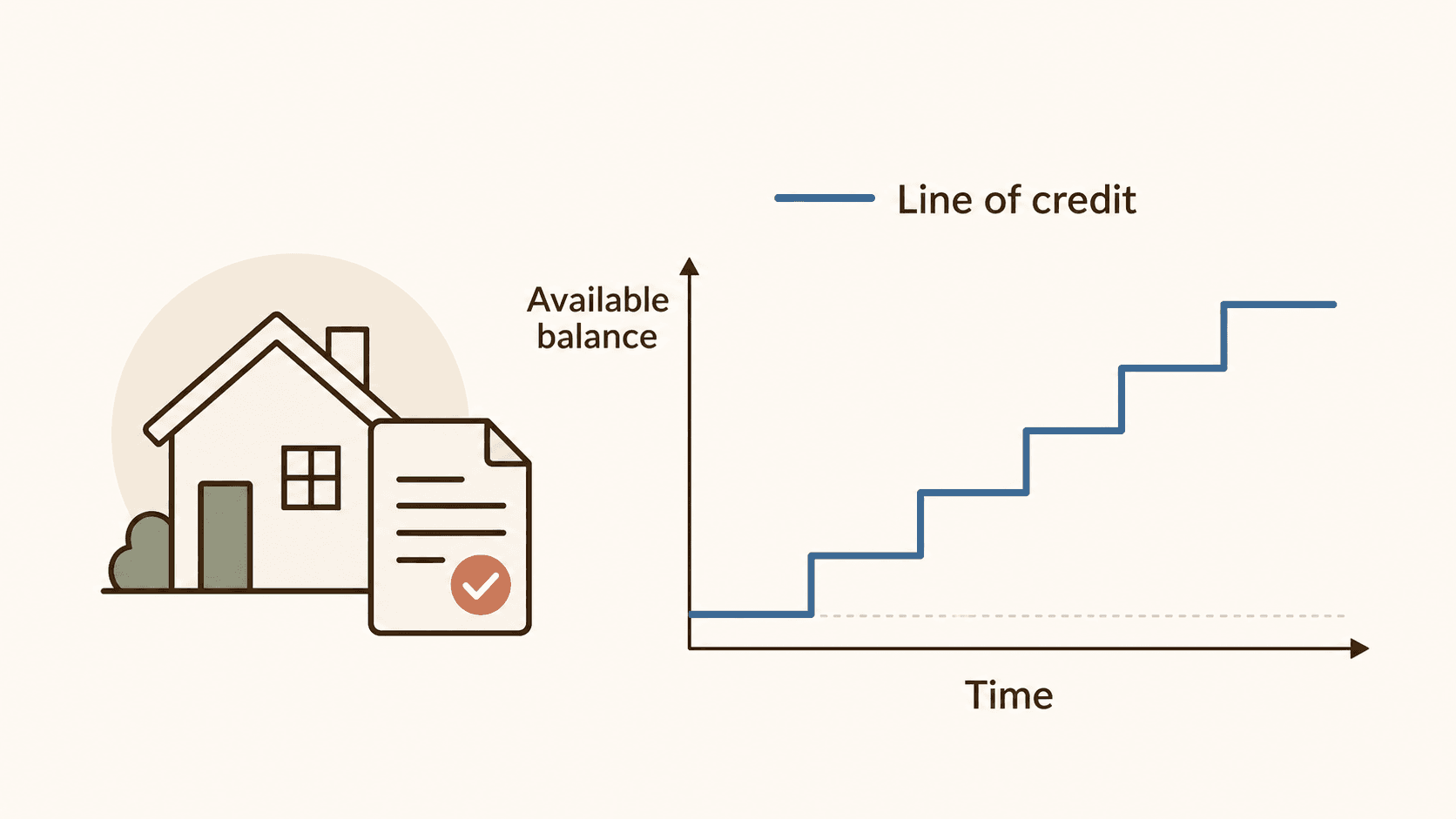

Line-of-credit growth is not interest earned by the borrower.

Non-recourse does not mean there are no responsibilities.

A HECM is not the same as a traditional forward mortgage.

The best payout option depends on goals, risk, and timing.

Questions to ask before applying

Would a line of credit, monthly advance, lump sum, or combination make the most sense?

How will the loan affect heirs and future sale plans?

Does the homeowner understand occupancy and property-charge obligations?

Should HECM for Purchase be compared with staying in the current home?

How HECM planning tends to show up in California

A HECM is the FHA-insured reverse mortgage program. For California homeowners, the important question is how the federal HECM framework applies to high-equity homes, existing mortgage balances, family expectations, and the desire to stay in place without rushing a sale.

Preserve time before a sale decision

Some California families use the HECM conversation to compare staying in the home with selling, downsizing, or drawing from other assets.

Create retirement cash-flow flexibility

A HECM may provide proceeds through available options such as a line of credit, monthly advances, lump sum, or a combination, subject to program and lender rules.

Coordinate adult children and heirs

Because California homes often carry meaningful equity, heirs should understand non-recourse protections, repayment, and future sale scenarios early.

HECM payout options to compare

The best structure depends on the homeowner's goal, available proceeds, current mortgage balance, family plan, and how long they expect to stay in the home.

Line of credit

May help homeowners keep flexibility for future needs, repairs, care costs, or timing around a later sale.

Monthly advances

May fit households trying to reduce pressure on retirement income while staying in the home.

Lump sum

May be considered when paying off an existing mortgage or solving a specific need, but it should be reviewed carefully.

Terms homeowners often ask about

Ask a question about hecm loans in California

Share the situation you are trying to solve. Ventana can help you understand whether the next step is a calculator estimate, a family conversation, counseling, or a deeper review.

Lori will review your note and follow up with a practical next step.

HECM Loans questions in California

What does HECM mean?+

HECM means Home Equity Conversion Mortgage. It is the FHA-insured reverse mortgage program for eligible homeowners.

What does non-recourse mean?+

Non-recourse generally means repayment is limited to the home's value when the loan becomes due and payable, subject to program rules.

Can HECM proceeds be taken as a line of credit?+

Many borrowers use a line of credit option, though available choices depend on loan terms, program rules, and borrower circumstances.

Official reverse mortgage references

Ventana explains reverse mortgage options in plain language. Program details should be confirmed against current HUD, FHA, CFPB, lender, and counseling guidance before a homeowner makes a decision.

Have questions about a reverse mortgage?

Talk with Ventana before you make a decision. The first conversation is about clarity, not pressure.