Reverse Mortgage FAQ in Arizona

Clear answers to the questions homeowners and adult children ask most often.

Short answer

The most useful reverse mortgage FAQ starts with ownership, repayment, heirs, eligibility, responsibilities, counseling, and alternatives.

What matters most in Arizona

A HECM reverse mortgage is federally insured and has program requirements.

The borrower keeps title to the home.

Heirs should understand repayment options before the family is under time pressure.

Counseling is required for FHA-insured HECM loans.

Common misunderstandings

Reverse mortgages are not free money.

A reverse mortgage is not only for people in crisis.

The home does not automatically become the lender's property.

FAQs should answer the question directly before adding nuance.

Questions to ask before applying

Who owns the home after closing?

What happens when the borrower passes away or moves?

How are heirs protected by non-recourse rules?

What costs and obligations continue after closing?

The questions Arizona homeowners usually need answered first

Arizona reverse mortgage questions often center on retirement cash flow, primary-residence rules, HOA or 55+ community obligations, snowbird plans, relocation, and whether HECM for Purchase should be part of the comparison.

Arizona eligibility and residence questions

Can a snowbird use an Arizona reverse mortgage?

A HECM is tied to the borrower's principal residence. Seasonal living should be reviewed carefully so the homeowner understands occupancy requirements before applying.

Do HOA dues still matter in Arizona?

Yes. HOA dues remain the homeowner's responsibility, along with taxes, insurance, maintenance, and occupancy obligations.

Can a 55+ community homeowner qualify?

Some may qualify, but property type, HOA obligations, occupancy, equity, age, counseling, and lender requirements all need review.

Relocation, purchase, and family questions

What is HECM for Purchase in Arizona?

HECM for Purchase may allow an eligible buyer to buy a primary residence using a HECM structure. It should be compared with buying with cash, using a traditional mortgage, or selling another home first.

Should someone moving from California compare HECM options?

Yes, if they are buying or relocating in Arizona. The comparison may include a standard HECM, HECM for Purchase, selling first, buying with cash, or choosing a different home.

Should heirs be involved?

Often yes. Heirs should understand repayment, future sale timing, the homeowner's housing plan, and how the reverse mortgage may affect family expectations.

Terms homeowners often ask about

Ask a question about reverse mortgage faq in Arizona

Share the situation you are trying to solve. Ventana can help you understand whether the next step is a calculator estimate, a family conversation, counseling, or a deeper review.

Lori will review your note and follow up with a practical next step.

Reverse Mortgage FAQ questions in Arizona

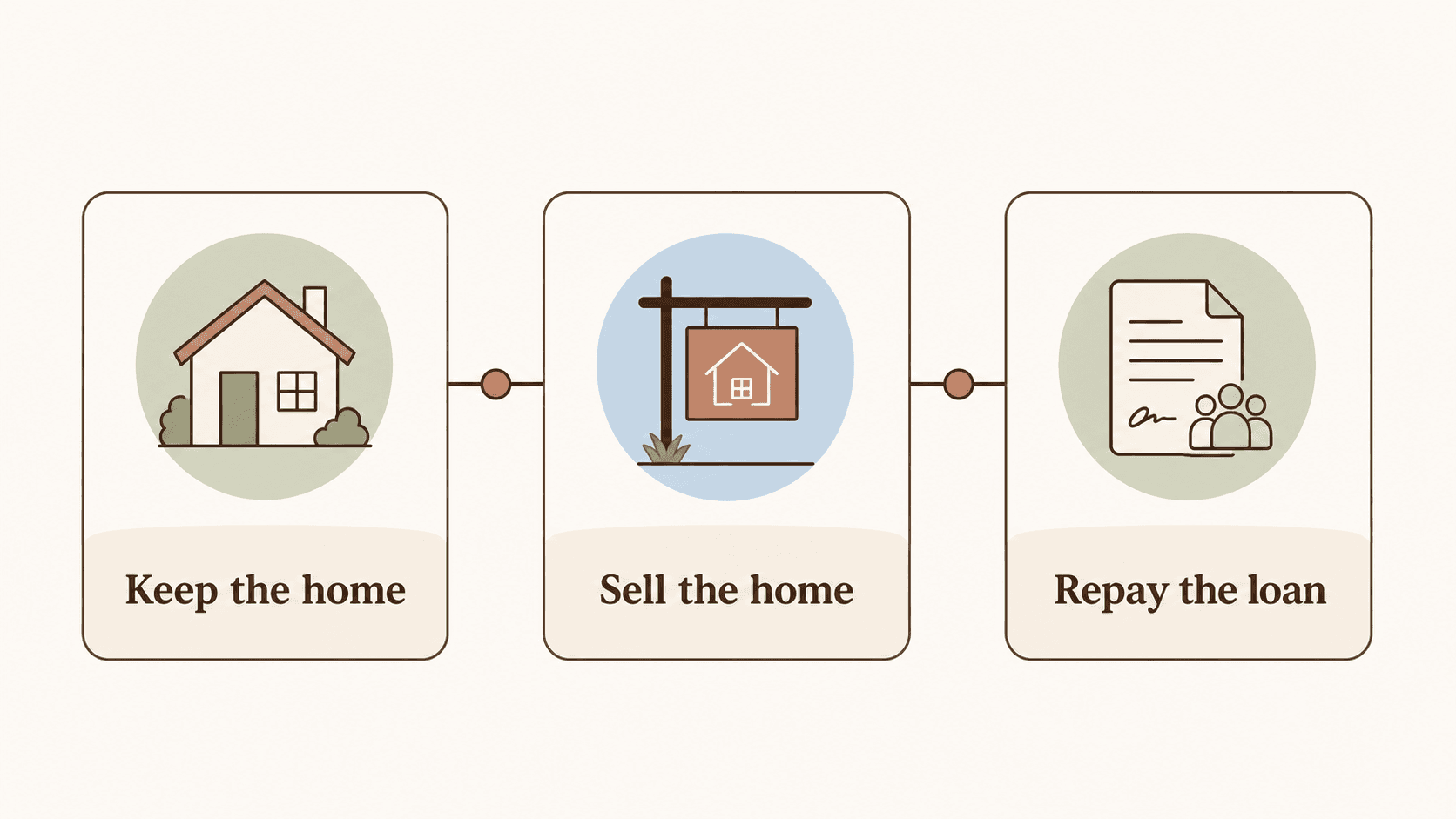

Can heirs keep the home?+

Heirs may keep the home by repaying the loan according to program and lender requirements. Many families also choose to sell the home and use sale proceeds to repay the loan.

Can reverse mortgage proceeds be used however the homeowner wants?+

Proceeds are often flexible, but the homeowner should use them in a way that supports the long-term plan and keeps required property obligations manageable.

Is counseling required?+

For FHA-insured HECM loans, counseling with a HUD-approved HECM counselor is required before moving forward.

Official reverse mortgage references

Ventana explains reverse mortgage options in plain language. Program details should be confirmed against current HUD, FHA, CFPB, lender, and counseling guidance before a homeowner makes a decision.

Have questions about a reverse mortgage?

Talk with Ventana before you make a decision. The first conversation is about clarity, not pressure.