Reverse Mortgage in Arizona

A reverse mortgage can turn part of a home's equity into funds while the homeowner continues living in the home.

Short answer

A reverse mortgage may help an eligible homeowner age 62 or older use home equity while remaining in the home, but the homeowner still keeps ownership responsibilities.

What matters most in Arizona

The home must remain the borrower's principal residence.

The homeowner must continue paying taxes, insurance, HOA dues when applicable, and maintenance.

The decision should be compared against selling, downsizing, refinancing, using investments, or waiting.

Adult children or heirs should understand how repayment typically works when the loan becomes due.

Common misunderstandings

The lender does not take ownership of the home.

A reverse mortgage does not remove property tax, insurance, maintenance, or occupancy responsibilities.

The right answer is not based only on available proceeds.

State pages should explain local context without pretending federal HECM rules are different in every city.

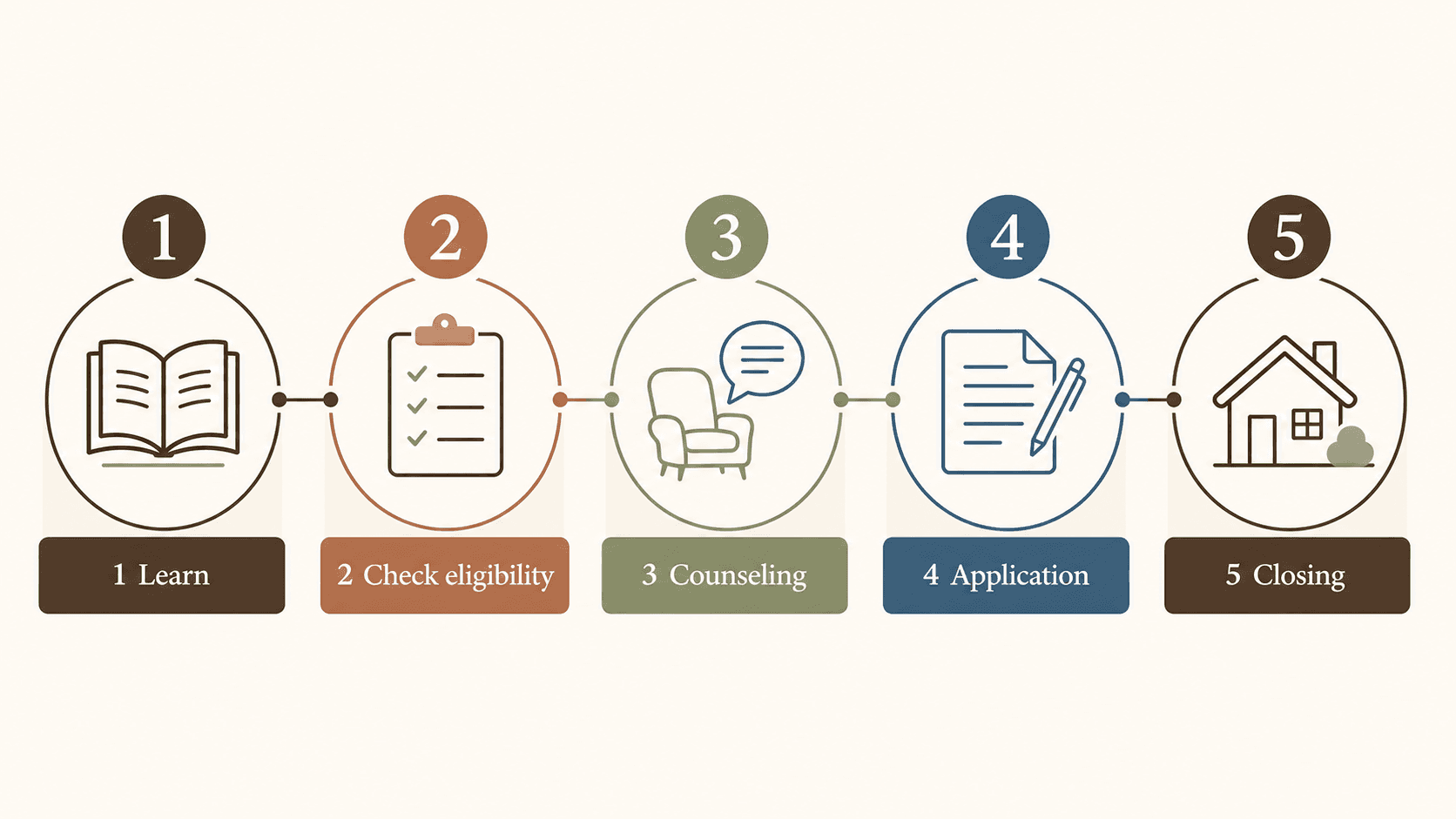

Questions to ask before applying

How long does the homeowner expect to stay in the home?

What problem is the reverse mortgage supposed to solve?

Can the homeowner keep required property charges current?

Have heirs or adult children been included if they will be affected by the decision?

The Arizona decision is local, even when the HECM rules are federal

For Arizona homeowners, the reverse mortgage decision often turns on retirement cash flow, HOA obligations, primary-residence rules, seasonal living, and whether the home still fits the next stage of life.

A retiree wants more predictable cash flow

The home may be comfortable and familiar, but fixed income, insurance, HOA dues, or care costs may be narrowing monthly flexibility.

A homeowner lives in a 55+ or HOA community

The conversation should include dues, property eligibility, maintenance expectations, and whether the community still supports the homeowner's long-term needs.

A family is comparing staying, buying, or relocating

Arizona decisions may include HECM for Purchase, moving from California, downsizing within Arizona, or keeping a seasonal lifestyle simple.

Reverse mortgage compared with other Arizona options

Main goal

Reverse mortgage

Use equity from the Arizona primary residence to support retirement flexibility.

Other option to compare

Downsize, relocate, buy with cash, use a traditional mortgage, or sell another home first.

Arizona planning issue

Reverse mortgage

HOA dues, occupancy, insurance, and seasonal residence questions need early review.

Other option to compare

Moving or buying differently may solve housing fit issues but can change community, care, and budget plans.

Family conversation

Reverse mortgage

Heirs should understand repayment and whether the home is expected to be sold later.

Other option to compare

A sale, move, or HECM for Purchase may be cleaner if the current home is not the long-term plan.

Terms homeowners often ask about

Ask a question about reverse mortgage in Arizona

Share the situation you are trying to solve. Ventana can help you understand whether the next step is a calculator estimate, a family conversation, counseling, or a deeper review.

Lori will review your note and follow up with a practical next step.

Reverse Mortgage questions in Arizona

Do you still own your home with a reverse mortgage?+

Yes. The homeowner keeps title and remains responsible for occupancy, taxes, insurance, HOA dues when applicable, and maintenance.

When does a reverse mortgage become due?+

A reverse mortgage generally becomes due when the borrower no longer lives in the home as the principal residence, sells the home, passes away, or does not meet required loan obligations.

Is a reverse mortgage right for every homeowner?+

No. It should be compared with other housing and retirement options, especially if the homeowner may move soon or cannot keep up with required property charges.

Official reverse mortgage references

Ventana explains reverse mortgage options in plain language. Program details should be confirmed against current HUD, FHA, CFPB, lender, and counseling guidance before a homeowner makes a decision.

Have questions about a reverse mortgage?

Talk with Ventana before you make a decision. The first conversation is about clarity, not pressure.